Exploring how two radically different investment philosophies lead to vastly different wealth creation outcomes.

1. Different Philosophical Approaches to Investing

The field of investment management encompasses a diverse spectrum of philosophical approaches and methodological frameworks, each with distinct implications for portfolio construction and risk management. Among these various strategies, market timing has emerged as a particularly prominent focus for many practitioners, who dedicate substantial analytical resources to predicting short-term market movements. This approach typically involves employing technical indicators such as Exponential Moving Averages (EMAs) to identify optimal entry and exit points, with the objective of avoiding market downturns while participating in upward rallies. This approach shifts focus away from fundamental analysis toward pure price variations and statistical patterns. While the allure of side-stepping every downturn is strong for many, history has repeatedly shown the immense difficulty of consistently predicting the market's short-term movements.

In this article, we argue that there is much more to be gained from identifying high-growth stocks (stock picking) than from attempting to time the market.

Furthermore, we believe the task of picking stocks is a much more rational endeavor to attempt.

History provides little evidence of successful long-term market timers, but it is filled with examples of good value investors

who were able to successfully analyze and select good companies based on sound fundamentals.

This data-driven comparison will be the focus of this article. So, how much more potential is there in stock picking?

2. Characterizing Investment Methodologies: From Timing to Selection

To evaluate the relative importance of stock selection versus market timing, we construct a conceptual framework that maps investment characteristics across these two critical skill dimensions. The matrix below illustrates how varying levels of proficiency in each domain combine to produce distinct performance profiles, from optimal success to complete failure.

| Good (High Alpha) | Neutral (Index) | Bad (Poor Selection) | |

|---|---|---|---|

|

Good Timing |

Optimal Success

Maximum alpha generation with perfect risk management

|

Pure Timing

Market returns enhanced by perfect entry/exit timing

|

Hindered Timing

Poor selection rescued by avoiding market downturns

|

|

Neutral (Always In) |

Pure Alpha

Superior selection drives returns without concern for timing

|

Market Returns

Standard buy-and-hold index fund performance

|

Underperformance

Poor selection leads to subpar long-term results

|

|

Bad Timing |

Hindered Alpha

Strong selection hindered by poor timing decisions

|

Timing Drag

Market returns reduced by mistimed entries/exits

|

Complete Failure

Poor selection compounded by mistimed market moves

|

Figure 1: Investment Approach Matrix

We conduct a conservative comparison of two specific buckets from this matrix: a skilled stock picker penalized with the worst possible timing versus a perfect market timer with no stock selection ability. We define two profiles based on this:

The Stock Picker ("Hindered Alpha")

This investor is dedicated to alpha generation, aiming to outperform the market index. Their success is rooted in deep fundamental analysis of a business's health and intrinsic value. This investor acknowledges that short-term price variations are often driven by factors unrelated to this value, such as general market noise or the speculative behavior of other actors. Therefore, they ignore this noise, focusing intently on selecting the right companies for the long term. Their success is determined solely by their stock selection skill.

The Market Timer ("Pure Timing")

This investor is defined by a singular focus: managing risk by predicting the market's direction. They hold no conviction in individual assets, opting instead to passively track a broad market index like the S&P 500. Their entire strategy is predicated on perfectly timing entries and exits, meaning their performance depends solely on this one skill: flawless market timing.

3. Isolating Variables

To determine whether stock selection or market timing offers greater potential reward, we will measure the maximum potential of each skill, isolating the ability in a controlled test.

To achieve this, we design the following experiment, built on two hypothetical scenarios. Each scenario represents the perfect,

ideal execution of one of these distinct skills. By creating these "perfect" but theoretical investor models, we can quantify the full,

theoretical impact of being a perfect stock picker versus being a perfect market timer.

A Thought Experiment

Let us consider the following scenarios, each representing a cell of the investing approach matrix defined previously.

Scenario A: The Stock Picker ("Hindered Alpha")

This investor possesses perfect stock-picking skill. Their strategy involves annually building an equally-weighted portfolio of the top 10 performing stocks within the S&P 500, guaranteeing significant annual alpha. To take a conservative approach, we deliberately pair it with the worst possible timing scenario: this investor is penalized by disastrous timing, being forced to miss the 10 best-performing days of the market each year.

Scenario B: The Market Timer ("Pure Timing")

This describes a passive investor who holds a portfolio tracking the S&P 500 (zero stock-picking alpha). Their edge is a crystal-ball type of oracel enabling Perfect Timing, allowing them to predict and entirely avoid the 10 worst-performing days of market (crashes/news) every single year, holding cash during these periods to preserve capital.

To summarize, each investor consults their oracle every January 1st: one identifies the best growth stocks, while the other anticipates the worst market days of the coming year. This comparison reveals whether fundamental stock selection can overcome poor timing, or if perfect market timing alone creates superior long-term wealth.

Note: this experimental setup is conservative since the Stock Picker is penalized with the worse possible timing, when one could use something closer to randomness, showing no skill in market timing.

4. The Results: Skill vs. Speculation

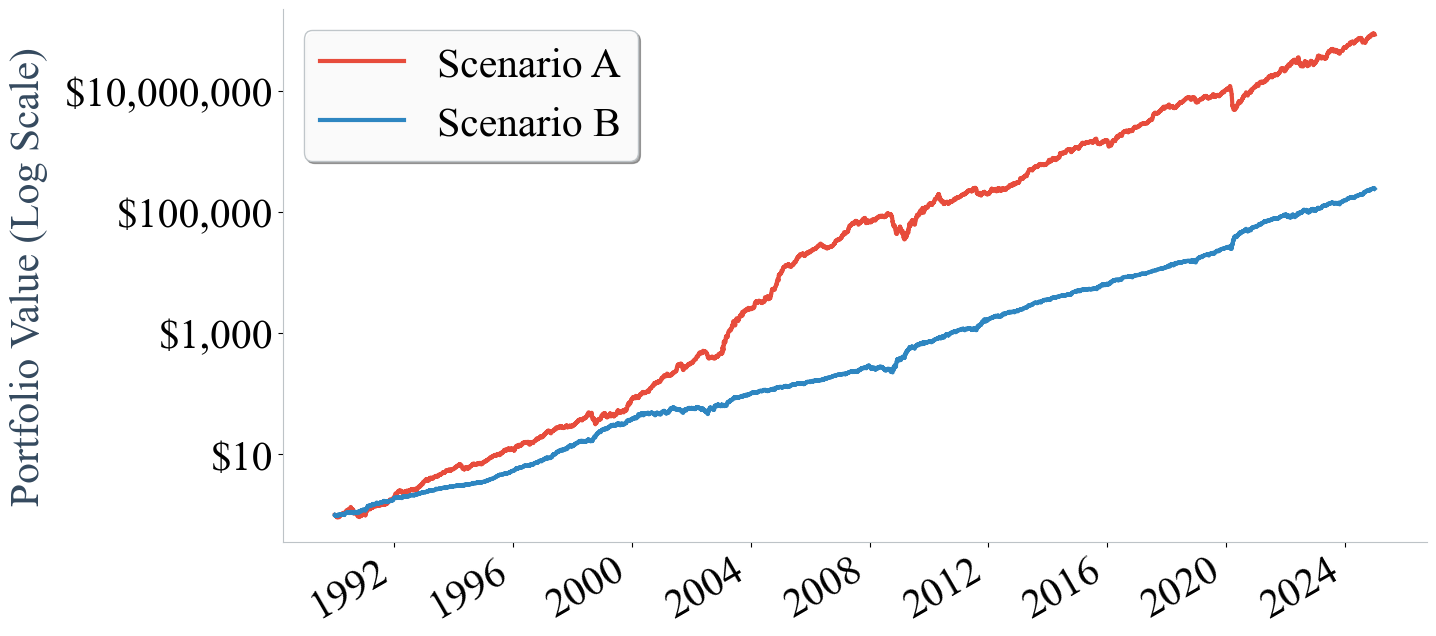

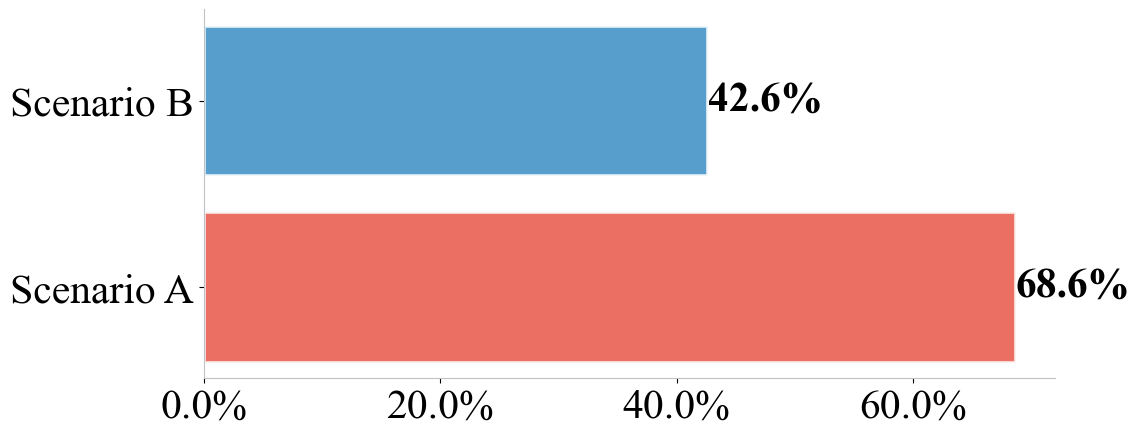

The results of our experiment are decisive: while Scenario B (Perfect Timing) achieved a strong 42.6% annualized return, it was completely overshadowed by Scenario A (Perfect Picking), which delivered an extraordinary 68.6% annualized return.

Figure 2: Portfolio Value Comparison

Figure 3: Annualized Returns Comparison

This highlights that high-quality stock selection is a dominant factor of wealth creation,

even when hindered by disastrous timing .

As visualized in Figure 2 and 3, the trajectory (log scale) of Scenario A dwarfs that of Scenario B.

This results show that under extremely penalized conditions the ability to pick the right stocks enables to significantly

outperform gains obtained through pure timing. As the penalty on the number of best days missed increases, it is naturally expected that the

stock picker will start underperfoming.

However, a poor picking ability is not compensated by a good timing capability : simulating returns obtained by an investor

randomly selecting 10 stocks every year (i.e., picking ability assimilated to randomness) while perfectly timing the market to avoid the 10 worst day every

year would yield an average 40.5% annualized returns, materially below the Stock Picker.

Note: this last comparison is still conservative as one could penalize the Market Timing by the worse possible picking skill,

as we did for penalizing the Stock Picker with worse possible timing.

The Lessons

This analysis offers evidence-backed frameworks to help investors choose their investment philosophy, clearly delineating the potential outcomes of different strategic approaches. From the results, we argue that principled investors should:

-

•Avoid the Timing Distraction

Attempting to predict short-term market movements, a task that has proven notoriously difficult, if not impossible, is a misguided allocation of an investor's time and effort.

-

•Focus on Fundamental Factors

The investor's focus should shift to the elements they can actually examine and study: business quality, valuation, and strong fundamentals.

-

•Understand and Avoid Emotional Decisions

A critical distinction must be made. Prudent risk management (like diversification or position sizing) is a necessary part of any strategy. Too often, however, investors engage in market timing disguised as "risk management" when it is actually just an attempt to manage their own emotions, namely, their fear of drawdowns. This reactive, fear-based approach should not be confused with a strategy that generates long-term alpha.

This is the core of our philosophy at Sabr Investment Technologies.

We put this belief into practice by focusing all our efforts on building strong selection skill. In line with our ethical mandate,

we avoid speculative timing and methods like shorting, rather we focus on understanding potential growth and associated risks, then commit to it.

Our process is not about reacting to fear of short term losses;

it is about building deep, fundamental and sound convictions while incorporating expected risk as a rational

input into our decisions from the very beginning.

Disclaimer

This content is provided for educational and informational purposes only and does not constitute investment advice, an offer to sell, or a solicitation of an offer to buy any securities or investment products. The information contained herein is not intended to be a comprehensive statement of approach and is subject to change without notice. Any investment involves risk, including the possible loss of principal. Readers should consult with their financial advisors before making any investment decisions. Nothing in this article should be construed as legal, tax, or financial advice. All information is provided on an "as-is" basis without any warranty of completeness, accuracy, or timeliness.